Open USD needs a weighbridge, not fewer partners

Samsung's denial was a symptom: nothing measures what a member is, and the fix is the machine that pays them.

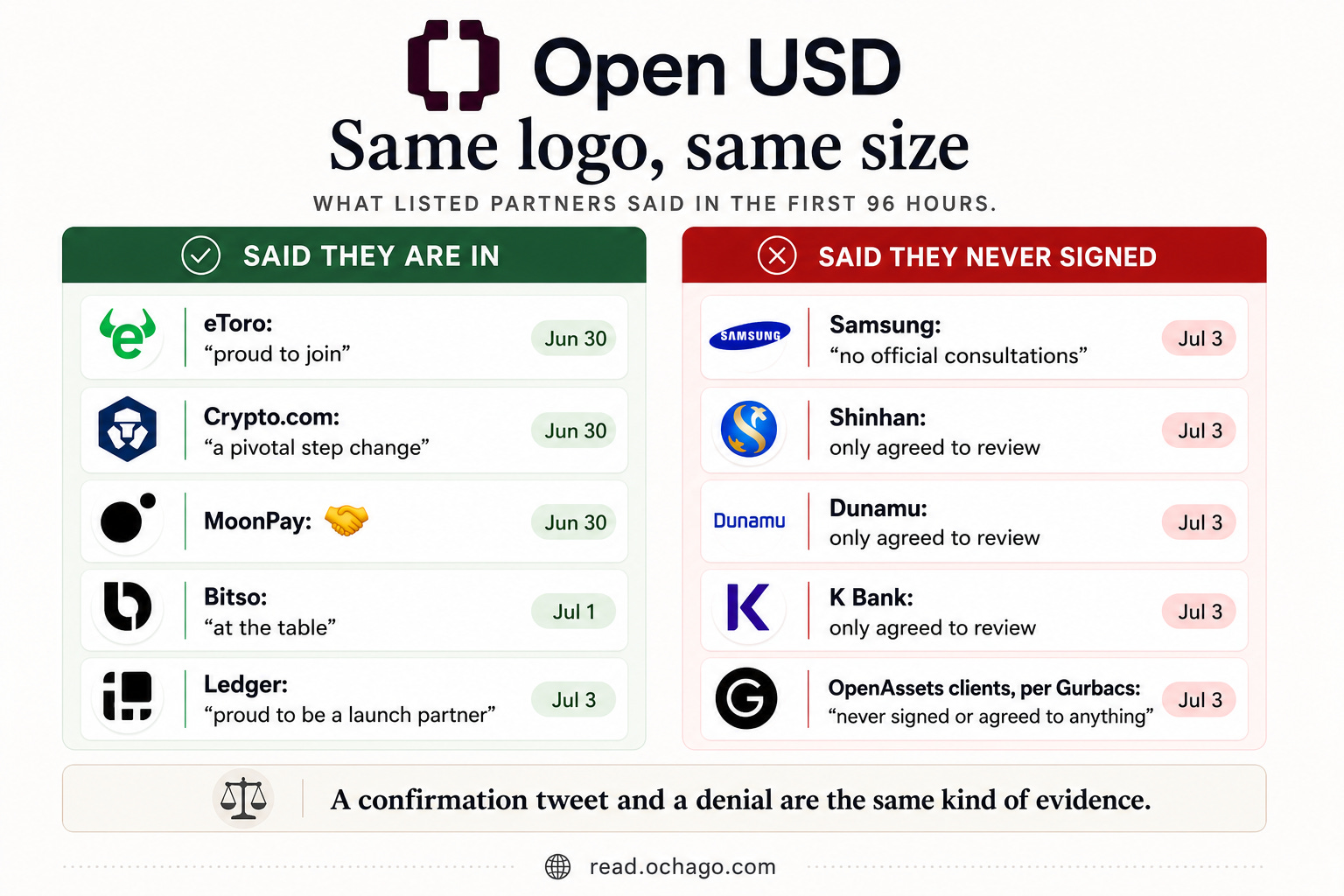

72 hours after Open USD launched with 140 partners, Samsung Electronics found out from Korean media that it was one of them.

I left one thread hanging in last week’s piece: Camila Russo asked what being a partner commits anyone to, and nobody on the launch page answered. I called governance the question I’d press first. I didn’t expect reality to press it inside a week. Chosun Biz reported that Samsung, Shinhan, Dunamu, and K Bank had signed nothing; Samsung said there had been no official consultations and it didn’t know what role it was supposed to play. Then Gabor Gurbacs checked with his own clients on the list and reported they “never signed or agreed to anything.”

The same list was confirming from the other side. eToro posted that it was “proud to join” as a launch partner within hours of the announcement. Crypto.com called it “a pivotal step change” the same afternoon, and MoonPay’s entire statement was a handshake emoji. Bitso put itself “at the table” for Latin America the next day, and Ledger was still posting “proud to be a launch partner” on the day the Korean denials spread. So the list holds companies loudly in and companies that never knew they were on it, wearing the same logo at the same size.

The easy read is a lying scandal, Protos ran exactly that headline, and it’s the read I’d caution against. What made me stop was the thought underneath both piles of statements: right now, the genuine members can’t prove they’re any different from Samsung. A confirmation tweet and a denial are the same kind of evidence. There is no unit for what a partner is.

What does joining weigh?

Recall the model. Open USD charges nothing to mint or redeem, and pays nearly all reserve interest to its partners based on the balances and volume they bring, and reserve interest is the entire prize; it was 99% of Circle’s 2024 revenue.

Think of a farm co-op that pays dividends by the grain each member delivers. Before that co-op needs more members, it needs a weighbridge. Open Standard published the member list before the weighbridge.

The law makes the weighbridge mandatory anyway, on both sides of the Atlantic. The GENIUS Act bars issuers from paying holders yield, and MiCA goes further, banning interest from issuers and even service providers across the EU. So in every market that matters, partner payments have to survive as documented compensation for measurable distribution work. The system that measures each partner’s contribution is the same system that makes the economics legal. One machine, two jobs, zero public evidence it exists yet.

Once you see it that way, “partner” stops being a status and becomes a rung. Six of them, and every rung above the first has an artifact nobody can fake:

L0, logo. A supportive conversation. Obligations: zero. Where Samsung was, involuntarily.

L1, paper. A signed membership agreement.

L2, sandbox. Mint and redeem keys live in testing.

L3, pilot. First attributed live volume. The dashboard line leaves zero.

L4, default. Open USD becomes a default option in one product line.

L5, treasury. Float policy changes; balances sit in the token.

The launch page flattened all six into one word. The denials were what that flattening looks like from Seoul.

Join is a different verb in every seat

Run the 140 through the ladder and a second structure appears. An acquirer settles in the token. A remitter routes through it. An exchange lists it. A platform pays out in it. A treasury holds it. A bank distributes it. A chain hosts it. Infrastructure enables it.

Only two of those verbs mint supply: holding balances and routing volume. Chains and infrastructure create capacity. Banks create legitimacy. Most of the list can’t convert in any way that shows up in supply, whatever they sign.

And the ladder climbs on lopsided economics. At a 4% reserve yield (substitute your own rate, the shape survives), $100 million of attributed average balance pays $4 million a year. That’s rounding error to a card network that already earns float on its own rails, and transformational to an African off-ramp or a LatAm remitter. So the mid-tail climbs fastest and the anchors sit low for structural reasons. Some are capped outright: Coinbase earns roughly half of USDC’s reserve income, and every Open USD balance on its platform would cannibalize a better deal. Its rational ceiling is a listing.

Where my first read breaks

Last week I told readers to watch where Open USD “shows up,” as if partners convert one at a time. That framing was wrong, and the miss is mine.

Work through any single member and you hit someone else. DoorDash’s launch statement points at exactly this, stablecoins as “a real path to bring that level of financial flexibility to other geographies we operate in”; a payout pilot in Nairobi or Mexico City needs a local off-ramp member live first. An off-ramp pilot dies on slippage unless someone seeds liquidity in the local pair. BBVA, the most enthusiastic bank on the page, legally can’t distribute the token in Europe until an issuer of record holds an e-money license, and none has been named. Nobody converts alone. The convertible unit is a corridor: one demand platform, one off-ramp, seeded liquidity, one license, switched on together.

That also softens a warning I made last week. I said that if the big members simply parked their own money in the token to make the supply chart look alive, Open USD would be a standard with no seller. Half right, and the half I missed is what parked money is for. A new corridor can’t carry its first real transfer until dollars already sit on both ends of it, because no remitter will route a customer’s money through an asset it can’t instantly buy and sell at size. Someone has to fund that pool before the first customer shows up, and in month one that someone is always a big member. It’s the cash in the till on opening day, not fake demand. The test is what the parked money is doing six months later. If it has become the float underneath real transfers, it did its job. If it’s still the only supply on the chart, it was a press release.

There’s a benchmark for what the honest version looks like. The one consortium dollar that grew, Paxos’s Global Dollar Network, went from 7 founders in November 2024 to 100+ partners and $1 billion of supply in 13 months, and it had a licensed issuer standing before the first logo went up. That’s the curve to beat and the order to copy.

What I’m watching

Grading last week’s shots first: governance answered itself in 72 hours, faster than I expected. Distribution stays open. New shots, written so I can’t wriggle out:

1. The unit. If Open Standard publishes membership tiers, or anything separating signed members from reviewers, before the token goes live, the list problem is repaired. If the next announcement is a bigger logo count, discount everything after it.

2. The license. If no US issuer of record and no EU e-money entity are named by go-live, members like BBVA stay decorative through 2027 and Europe keeps belonging to whoever holds the paper, which was last week’s MiCA point and it stands.

3. The first corridor. If the first non-seed volume is a platform payout corridor with a local off-ramp member attached, the incentive design works. If supply at month 6 is still mostly anchor treasuries, my parked-supply warning graduates from caution to verdict.

4. The Coinbase rung. If Coinbase ever moves Open USD past a listing into any default placement, my ceiling argument is wrong and I’ll say so here.

5. The benchmark. USDG reached $1 billion in 13 months. If Open USD, with 20 times the launch surface, is under that pace at month 13, the consortium’s size was marketing and the weighbridge never got built.

The denials will be forgotten by August. The measurement problem won’t be, because the yield can’t legally be paid without it and the members can’t be real without it. A logo is a claim. A balance is a fact.

I write about money and technology from the emerging-market edge, after a decade building market entry and payments across Africa, including one of the continent’s first fiat-to-crypto gateways and ecosystem growth for a major Layer 2. I hold no position in CRCL or any token named here. Figures are from Open Standard’s launch materials, Chosun Biz via the reporting linked above, and Paxos’s Global Dollar Network releases. Open USD’s supply, tier contracts, and yield formula aren’t public; those are gaps, not guesses. One operator reading a launch list against a rulebook. Not investment advice.