140 companies launched a neutral dollar (OUSD). One of them runs it

Open USD lands the same week MiCA reshapes Europe's dollar market. The model is clever. Whether the members holding the real distribution ever use it is the whole question.

On Tuesday 30th June, 140 of the largest companies in finance and technology launched a new dollar and called it neutral.

Several of them already issue their own.

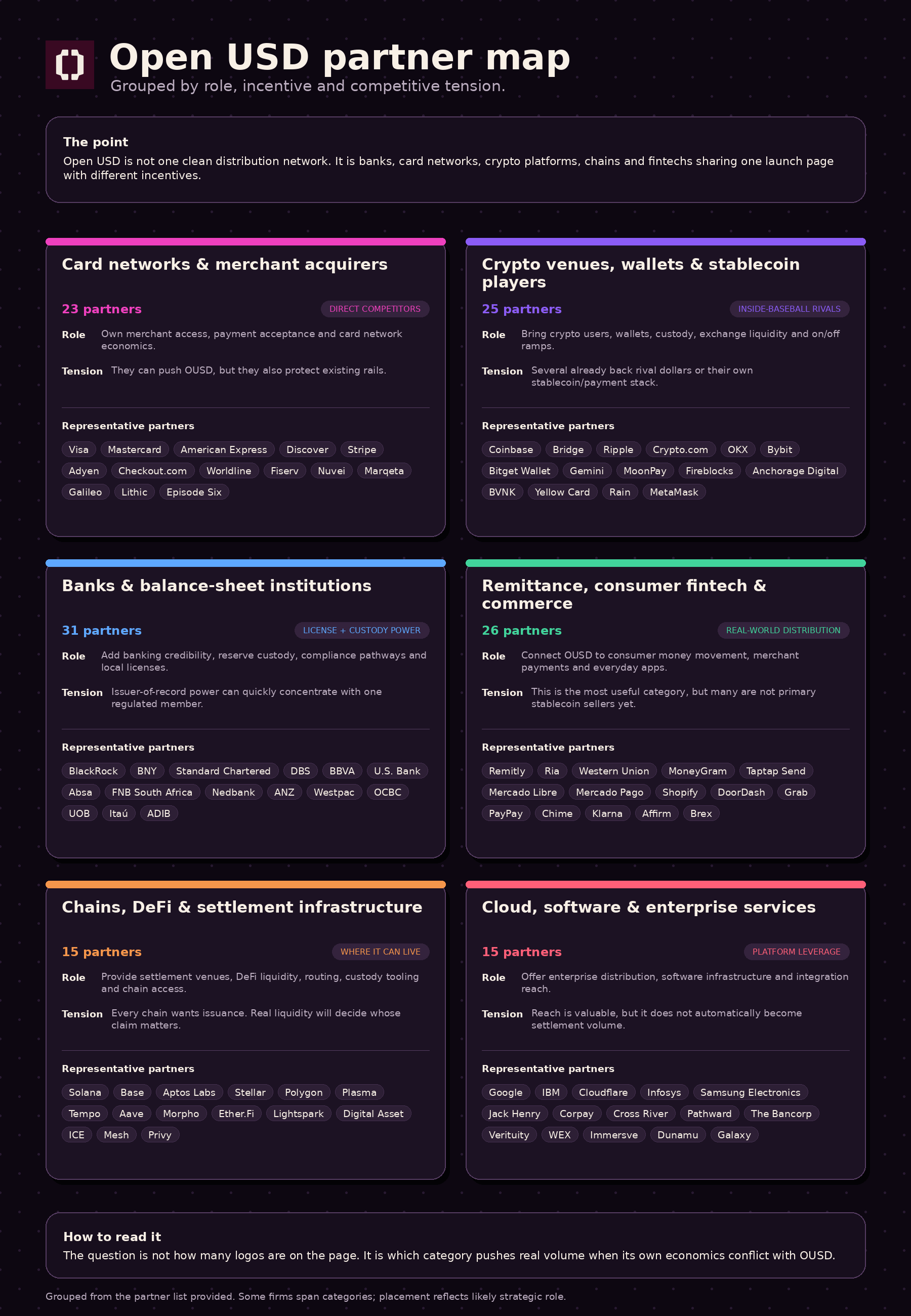

Visa, Mastercard, Stripe, Coinbase, BlackRock, Google, Ripple, and more than 130 others put their names on Open USD, a stablecoin governed by its members instead of one issuer. A launch like that only happens when the prize is big enough to make rivals share a table. So start with the prize.

Stablecoins settled about $9 trillion last year, more than half of what Visa moved (a16z, adjusted for wash trading). More than 1% of all US dollars now exist as tokenized stablecoins, collectively the seventeenth-largest holder of US Treasuries. Add the GENIUS Act last July and Circle’s IPO, and the market finally had both things it always lacked, a legal container and institutional validation.

So the open question stopped being whether dollar stablecoins matter. It became who controls the standard they run on. This week handed back two answers, one from a regulator and one from a coalition.

Europe answered first, by deadline

On July 1, MiCA’s transition window closes across the European Economic Area, and USDT effectively disappears from regulated EU venues. Tether never applied for the e-money authorization the rule requires, so its dollar is no longer compliant on any licensed European exchange. The delistings have rolled out for over a year.

USDC kept its listings because Circle holds an EMI license out of France and can passport the token across the bloc. The scoreboard already moved: USDT volumes on EU venues fell more than 70% between late 2024 and mid-2025, while USDC’s roughly doubled. Regulation did not threaten a shift in Europe. It forced one, and USDC won not on product but on paperwork, by holding the license its largest competitor would not file for.

That also sets the bar for whatever launches next. To operate across Europe a stablecoin needs a single licensed issuer of record, one named entity holding the e-money authorization. That rule is about to meet a dollar with 140 owners and no single one. Hold that thought.

Then the coalition answered

The same day, Open Standard launched Open USD, and the guest list is the whole story. Read it grouped by interest instead of by logo and the neutrality wobbles. The card networks, Visa, Mastercard, American Express, are each building their own tokenized settlement. Coinbase earns roughly half of USDC’s reserve income from a deal with the issuer this is built to undercut. Stripe runs its own stablecoin, USDB, through Bridge, whose co-founder, Zach Abrams, now runs Open USD. And the crypto names brought dollars of their own: Ripple has RLUSD, Gemini has GUSD, Aave has GHO. A neutral dollar, backed by a coalition of companies that mostly issue or earn from competing ones.

Ripple is the one I keep staring at. It joined as a day-one integration partner, positioning the XRP Ledger as a rail Open USD can settle on, while it already issues RLUSD, most of which, as I wrote a month ago, does not even live on the XRP Ledger; it migrated to Ethereum. So Ripple is plumbing a rival dollar while its own shrinks on a competitor’s chain. That stops being a contradiction once you read Ripple not as a stablecoin issuer but as a company that wants to be the toll road no matter whose car is on it.

The economics are a deliberate inversion of the model that just won Europe. A stablecoin issuer makes its money on the float: it parks the reserves in Treasuries and keeps the interest, which was 99% of Circle’s 2024 revenue. Open USD charges no mint or redeem fees and hands nearly all of that interest to the partners who distribute it instead. It goes live later this year on several chains at once, Solana, Stripe’s own Tempo, Base, Stellar, Polygon, each claiming day one, which is its own tell about who is steering. The market read it fast: Circle’s stock fell about 15%, its worst day since February, on a model built to drain the revenue line that is nearly all of its business. Whether that was an overreaction is fair to ask, an earlier consortium dollar with the same pitch never dented USDC, but the market plainly read the threat as real.

The cheering was immediate. The colder voices were worth more. Camila Russo noted that many of these 140 compete head to head, then asked the unglamorous question: what does being a partner commit you to, a binding agreement to carry Open USD, or a name on a launch page. Nobody on the page answered it. One onlooker put it as a joke: everyone signed up, and no one is quite sure what they signed up for.

Neutral is a negotiation, not a design

Here is where I slow down, because I have built the kind of distribution this depends on, and an org chart is not an operating reality.

The reserve-sharing model is genuinely smart. It fixes the oldest problem in stablecoins, that nobody runs hard distribution for a dollar they do not earn on. Pay the distributors and everyone has a reason to push. On paper.

In practice, the members with the best distribution have the least reason to use it, with one loud exception. Coinbase earns roughly half of USDC’s reserve income through its Circle deal; Visa and Mastercard are building their own rails. None will push a dollar that eats a margin they already collect. For a Shopify or a Samsung, with no competing product, the math is easy; for the anchor distributors, Open USD has to out-earn what they already make first, and mostly it will not.

The exception is Stripe, and Stripe is the tell. It is making Open USD the default for businesses on its platform, the Bridge co-founder runs the consortium, and one of the day-one chains is Stripe’s own Tempo. Stripe is not dragging its feet, it is steering, and it still issues USDB and runs Bridge’s platform for anyone else who wants to mint their own. So the most committed member of a neutral coalition supplies its chief executive, its default placement, a launch chain, and a competing dollar of its own. That is not neutrality. That is a host.

And look at who is not in the room. The corridors where a cheaper dollar changes something are Nigeria, Kenya, the Philippines, Indonesia. The global banks are there, Standard Chartered, DBS, BBVA, but the last-mile rails that move money in those markets, the mobile-money operators and African fintechs, are not. Open USD launches with enormous reach where Visa and Swift already reach, and thin presence where they do not. I have sat in enough central-bank meetings to say it plainly: a dollar’s distribution is decided one license and one local partner at a time, and that work is not on a launch page.

Abrams reached for the comparison himself: financial services needs this the way mobile needed Android. It is a more revealing analogy than he intended. Android is open the way the biggest player in the room allows it to be.

What I’m watching

Two things, written down so I cannot move the goalposts later.

Governance. The risk is not that 140 companies cannot agree. It is that the inner circle does not have to. When a handful of anchor members have overlapping ambitions, the standard drifts toward whatever the strongest distributor can quietly route around, and today that is Stripe. A neutral dollar the largest member can ignore when it conflicts with its own product is not open, it is Stripe-tolerant. Diem had 28 members and collapsed when its partners hedged rather than committed; this has five times the surface area. William Blair’s analysts called it a solution searching for a problem and doubted 140 rivals will agree on anything quickly or fund a zero-profit network for free; others called it a cartel to commoditize issuance. And MiCA makes it concrete: a stablecoin needs one licensed issuer of record. So who is Open USD’s? If no member holds the license, it cannot passport the bloc; if one does, the coalition just handed legal control to a single competitor. Governance and compliance are the same question, the one I would press first.

Distribution. Watch where Open USD actually shows up. If it lands first in boring, non-crypto enterprise corridors, where the member pushing it has no competing dollar, the incentive design is working. If a year out the supply is mostly anchor-member treasuries parked to make the launch look alive, the coalition built a standard with no seller.

The question was never whether tokenized dollars become a primary settlement layer; nine trillion dollars settled that. It is who controls the distribution, and this week handed back two partial answers. In Europe, a regulator chose, and it chose the issuer with the license. Everywhere else, 140 companies tried to choose by committee, with a model that pays everyone to agree. A neutral dollar designed by the incumbents it is meant to neutralize is not a revolution. It is a truce. And truces hold exactly as long as everyone’s interests point the same way. I would watch the first market where they don’t.

I write about money and technology from the emerging-market edge. Over the last decade I’ve built market entry and payments across Africa, including one of the continent’s first fiat-to-crypto gateways and ecosystem growth for a major Layer 2. I hold no position in CRCL, USDC, USDT, or any token named here. Figures are from a16z’s State of Crypto report, Open Standard’s launch materials, and the reporting linked above. Open USD is not yet live, and a launch coalition is not active distribution, which is flagged here rather than glossed. One operator reading a launch page and a regulatory deadline on the same afternoon, not investment advice.