Ripple built the XRP Ledger for payments. Its own dollar moved to Ethereum.

Ripple spent a decade building the XRP Ledger as the home for its assets. Today most of Ripple's own stablecoin sits on Ethereum, the chain it competes with. That migration is what distribution actual

Ripple has spent more than a decade building the XRP Ledger and telling the market it’s the chain built for moving value. So here’s the fact that stopped me when I pulled the data this week: most of Ripple’s own dollar doesn’t live there.

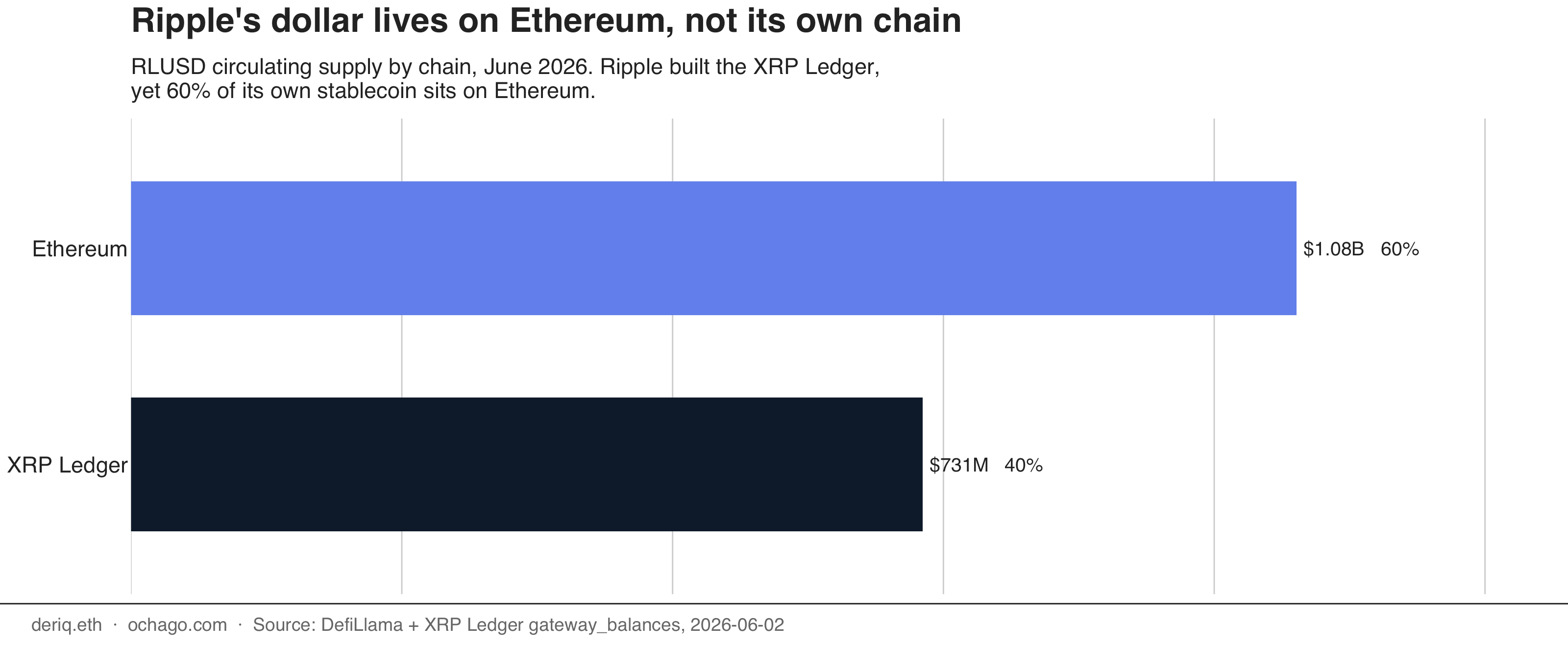

RLUSD has about $1.81 billion in circulation. Of that, roughly $1.08 billion sits on Ethereum and $731 million on the XRP Ledger (DefiLlama per-chain data, which matches a direct read of the issuer’s on-ledger balances on the XRPL to the decimal, June 2, 2026). Sixty percent of the stablecoin Ripple issues is on Ethereum, the chain Ripple has positioned against for years. The dollar moved to the neighborhood Ripple doesn’t own.

I don’t read that as a stumble. I read it as the most honest thing in the whole RLUSD story, because of where the rest of the spending is going.

The dollar follows the distribution

A stablecoin lives where its distribution is, and Ripple is buying distribution into institutions, hard. In January it put $150 million into LMAX Group and signed a multi-year deal to make RLUSD a core collateral and settlement asset across LMAX’s institutional venues, spot crypto through perpetual futures and CFDs. LMAX ran $8.2 trillion in institutional volume in 2025. In May, Copper, one of the larger institutional custodians, added RLUSD to its platform and to a yield program for the funds that custody there. And the institutional money, the prime-broker collateral, the DeFi venues, the integrations that LMAX and Copper plug into, all of that lives on Ethereum and its EVM cousins, not on the XRP Ledger.

So the supply split is the receipt of a distribution strategy, not a popularity contest between two chains. Ripple is paying to wire RLUSD into the places institutions already operate, and those places are EVM-native, so the dollar pools where the integrations are. Sixty percent on Ethereum is what it looks like when an issuer chases institutional rails instead of defending its own chain.

That pattern shows up in my own backyard too. Ripple’s custody technology went into Absa Bank in October 2025, one of Africa’s largest banks, Ripple’s first major bank-custody partner on the continent, serving institutional clients across roughly a dozen countries. People will file that under “Africa story,” but it’s the same move as LMAX and Copper, pointed at a different institution: sell the rails the money already runs on. The throughline is a customer, not a region, and the customer is the institution.

What distribution actually takes

I spent the last few years running ecosystem and distribution growth for Base, so this is the part I can say with some authority: an issuer does not get to choose where its token lives. The integrations choose. You can mint on whatever chain you want, but the supply gravitates to wherever the wallets, the venues, and the collateral engines already are, and getting into those is slow, expensive, one-counterparty-at-a-time work that almost nobody outside the function sees.

Ripple had the option most issuers would kill for. It owns a chain. It could have forced RLUSD onto the XRP Ledger, pointed at a big on-ledger number, and called it adoption. It didn’t. It went where the institutions were, which meant Ethereum, and it paid for the privilege, $150 million into a single venue is not a press release, it’s a budget. That’s the unglamorous truth of distribution: you go to the user. The user does not come to you, no matter what chain you built for them.

So what is the XRP Ledger for

The 40 percent on XRPL isn’t dead weight, and the supply number alone won’t tell you what it’s doing. So I pulled the on-chain activity for both chains to see how the dollar actually moves. It moves in opposite ways.

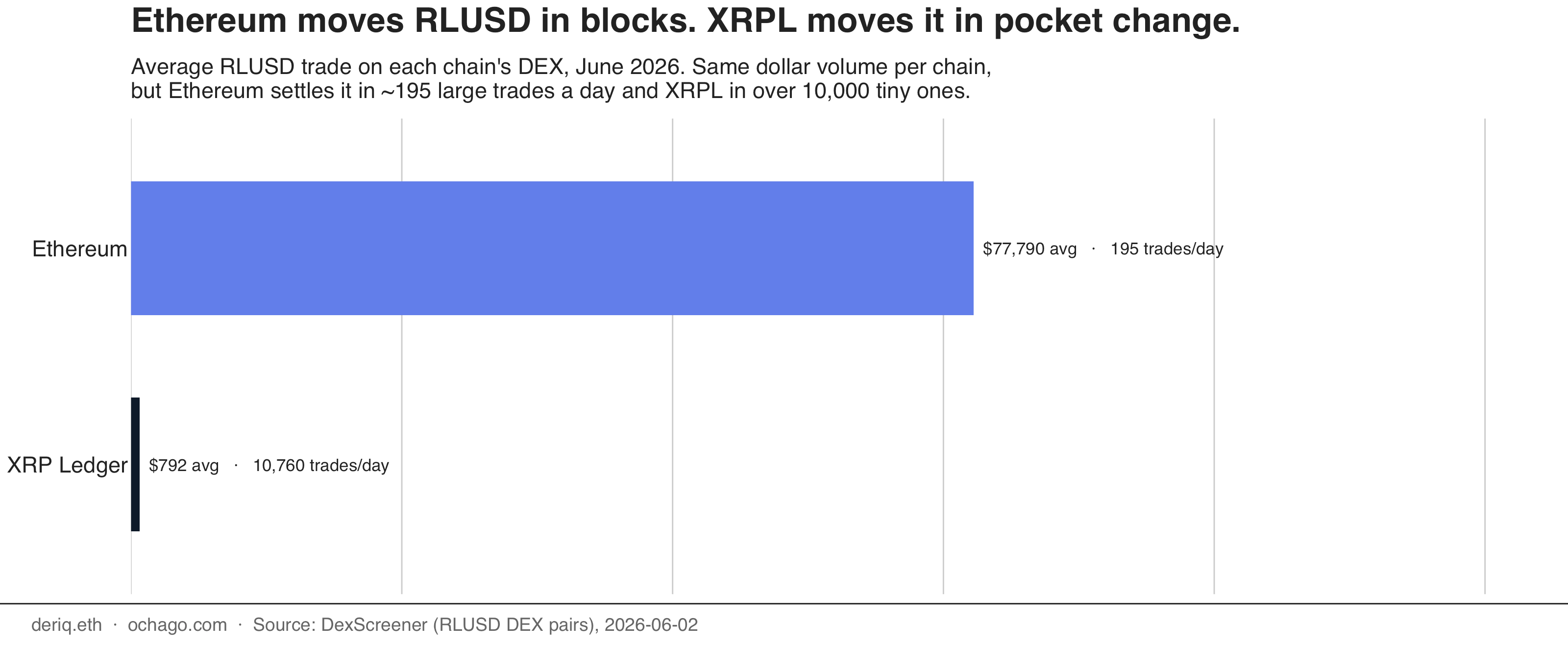

On Ethereum, RLUSD changed hands across about 8,800 transfers in the last seven days, roughly 1,250 a day (Dune, reading the ERC-20 transfer logs). On the trading side it does around $15 million of DEX volume a day, but across just 195 trades, an average of about $78,000 each (DexScreener, June 2). That’s institutional-size: a handful of large blocks, RLUSD against USDC on Uniswap and Curve. The XRP Ledger does a comparable $8.5 to $9.6 million of DEX volume, but across thousands of small trades. DexScreener counts 10,760 of them at about $790 each; On The DEX, the XRPL-native tracker, counts more still, over 25,000 trades across eighteen pairs at roughly $380, traded against a basket that includes XRP, Brazilian real, yuan, and USDC (On The DEX). Same dollar, two different motions: big and rare on Ethereum, small and constant on XRPL.

That answers the velocity question I walked in with, and not the way I expected. Normalize each chain’s trading to the supply sitting on it and the two come out close, Ethereum turning over about 1.4 percent of its balance a day and XRPL roughly 1.2 to 1.3 percent. The comfortable story, that XRPL is the fast settlement rail doing the real work while Ethereum just parks the balance, isn’t what the numbers say. Per dollar of supply the two chains move at nearly the same speed. Where they split is ticket size, and ticket size is the tell. The large institutional blocks, the collateral and custody balances that LMAX and Copper plug into, settle on Ethereum, where the average RLUSD trade is a five-figure sum. The high-frequency, small-denomination work, thousands of sub-$400 trades a day against a basket of currencies, runs on XRPL, the payments-and-FX profile the ledger was built for. One chain is the vault. The other is the cash register.

One honest limit on that read. What I measured is DEX trading, the order books on each chain. Pure peer-to-peer payment settlement on XRPL, wallet to wallet and outside the DEX, isn’t queryable without running a full ledger node, and when I read the issuer’s own transaction history it came back almost entirely market-making orders, not payments. So XRPL’s true settlement number sits somewhere above what I can see here. But the burden of proof was on the idea that the XRP Ledger moves the dollar faster, and the visible data leans the other way. What the ledger clearly is, for its own home dollar, is busier and smaller.

What I’m watching

Three things from here.

First, the direction of the migration. In December 2025 Ripple announced RLUSD’s move to four Ethereum layer-2s, Optimism, Base, Ink, and Unichain, issued natively across them through Wormhole’s transfer standard. It hasn’t shipped on-chain yet, the rollout is still in testing and waiting on NYDFS sign-off, which is why the live supply is still only Ethereum and the XRP Ledger. But all four are EVM rollups that settle back to Ethereum, so when they go live they add to the Ethereum side of this split, not the XRPL side. The announced direction is more EVM, not a turn back to the home chain.

Second, ticket size over time. Today Ethereum is where the large blocks settle and XRPL is where the small, frequent trades run, the vault and the cash register. If RLUSD is going to be a payments dollar and not just an institutional one, the bigger tickets should start showing up on the XRP Ledger too, not only on Ethereum. I’ll be watching whether the average XRPL trade creeps up, or whether the two chains stay split the way they are now.

Third, and this is the strategic one, what the XRP Ledger is becoming to Ripple’s own dollar. The busy retail and currency-trading layer, thousands of small tickets a day, while the institutional weight settles on Ethereum? For a company whose entire identity is its ledger, that’s not a small question. The dollar already voted with its feet. The question is whether Ripple admits where it walked.

Disclosure: I previously led Africa and Ecosystem Growth for Base at Coinbase. I hold no position in RLUSD, XRP, or Ripple as of writing. Supply figures are direct reads from DefiLlama‘s per-chain data and the RLUSD issuer’s on-ledger balances on the XRP Ledger. Activity figures are mine: a Dune query on Ethereum transfer logs, and DexScreener plus On The DEX for per-chain DEX volume and trade counts. All as of June 2, 2026; deal terms are from the reporting linked above. Pure peer-to-peer payment settlement on the XRP Ledger outside the DEX isn’t cleanly queryable without running a full ledger node, and is flagged as such in the piece, not estimated. One operator reading the on-chain data, not investment advice.

This was a shorter read than the last one and easier for me to follow. I found the direction of migration interesting. So was the aspect of a vault vs a cash register.

Keep sharing these. They are informative and stimulating. I learn something fascinating each time.