USDC grew $18.6 billion in 12 months. The Africa story was a single wallet.

The chain-by-chain breakdown reveals a 49-point gap between global USDC growth and the Africa-aligned chain. Three moves could close it. None of them require a new product.

USDC‘s outstanding supply grew $18.6 billion in the last twelve months. The single Africa-aligned chain in the dataset went the other way.

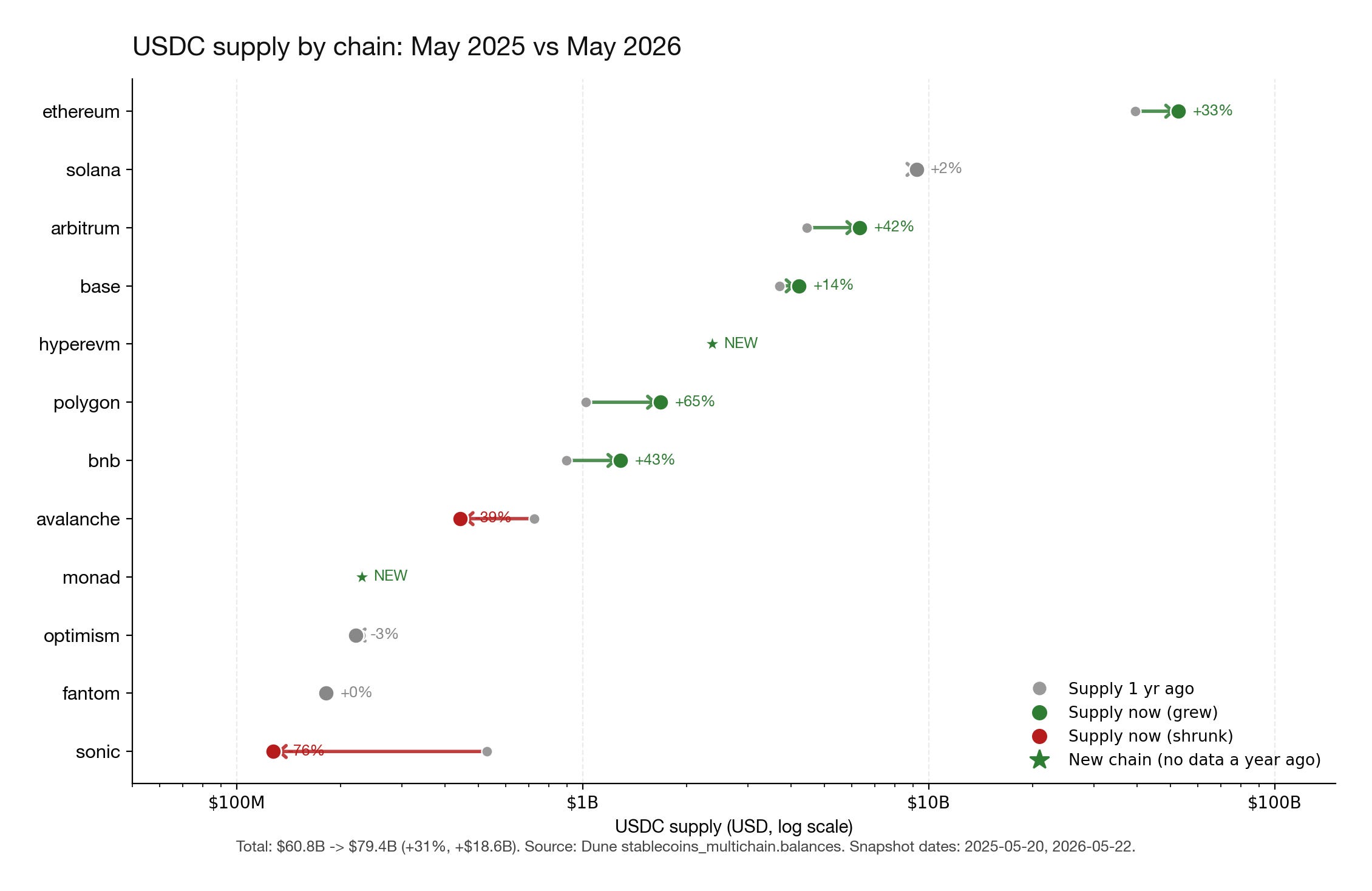

That was the line that made me stop and pull the chain-by-chain breakdown. Circle just shipped its biggest year on the product side, with USDC supply going from $60.8 billion to $79.4 billion and unique holders nearly doubling. The chart should be a clean victory lap, and from a global view it is. But the moment you split it by chain, the question gets interesting fast. Where did the new $18.6 billion actually land, and why did almost none of it land where Africans transact?

What USDC actually did this year

Headline numbers, all from the same Dune snapshot. USDC outstanding supply: $60.8 billion to $79.4 billion, up 31 percent. Unique on-chain holders: 25.4 million to 46.7 million, up 84 percent. So the holder curve grew almost three times faster than the dollar curve, which means each new wallet on average holds less USDC than the average wallet a year ago. That’s exactly the shape of a consumer crypto adoption curve. People joining the network, not whales accumulating.

A note on the market reaction. CRCL closed at $114.21 on May 22, 2026, against a 52-week high of $298.99 and a $31 IPO price. That’s a 62 percent drawdown from the peak against a product that grew 31 percent in the same window. The divergence sounds stunning until you read Circle’s S-1.

Per the filing, Coinbase receives 100 percent of the interest income from USDC held directly on its platform, and 50 percent of the residual reserve income from USDC held off-platform. In 2024 Circle generated about $1.7 billion in revenue and paid roughly $908 million of it to Coinbase as distribution costs. Net income for the year was $156 million. So a meaningful share of every dollar of "USDC supply growth" you see on the chart accrues to Coinbase, not to Circle. The other half of the bear case is the Fed, which cut aggressively through 2024 and 2025 and now sits at 3.5 to 3.75 percent, compressing the absolute reserve pool that the revenue share divides up. The supply growth is real. The Circle-side economics of that growth are much smaller than the headline suggests.

What the data is telling me

Ethereum is still the anchor, and added the most supply in absolute terms. $39.5 billion to $52.8 billion, an extra $13.2 billion. Two-thirds of all USDC supply lives on Ethereum mainnet. The “USDC is migrating to L2s” narrative people keep repeating isn’t actually in this data. USDC isn’t migrating. It’s growing everywhere, and Ethereum is growing fastest in dollar terms.

Arbitrum was the fastest-growing big chain at 42 percent. Polygon grew 65 percent. BNB Chain grew 43 percent. HyperEVM, Hyperliquid’s chain, came from a zero balance one year ago to $2.37 billion across only 43,000 wallets. An average of $55,000 per holder. That’s institutional perpetuals-desk margin parked in USDC.

The interesting break is Base. Supply grew only 14 percent there, $3.7 billion to $4.2 billion. But the holder count went from 2.8 million to 9.4 million, a 238 percent jump. Base now has more USDC wallets than Ethereum mainnet despite holding twelve times less in dollars. The average Base wallet holds about $447 in USDC. That’s a real consumer product, mostly running through Coinbase Wallet and the Base ecosystem apps. It’s the most interesting consumer USDC growth in the entire dataset, and it happened almost entirely on the chain Coinbase controls end-to-end. The mechanic stacks. The 50 percent reserve-income share Coinbase gets from Circle is a global pool, applied to all USDC supply wherever it sits, including Base. The Base sequencer revenue, about $19 million gross in Q4 2025 per Coinbase’s shareholder letter, is Base-only. So USDC growth on Solana benefits Coinbase through the reserve share alone. USDC growth on Base benefits Coinbase through the reserve share AND the sequencer fee on every transfer. Circle benefits too. It benefits less.

Then the losers, all of them double-digit. Avalanche down 39 percent. Sonic down 76 percent. Unichain down 74 percent. ZKsync down 78 percent. USDC isn’t just growing. It’s consolidating onto the chains that actually have users.

Where it’s hitting friction

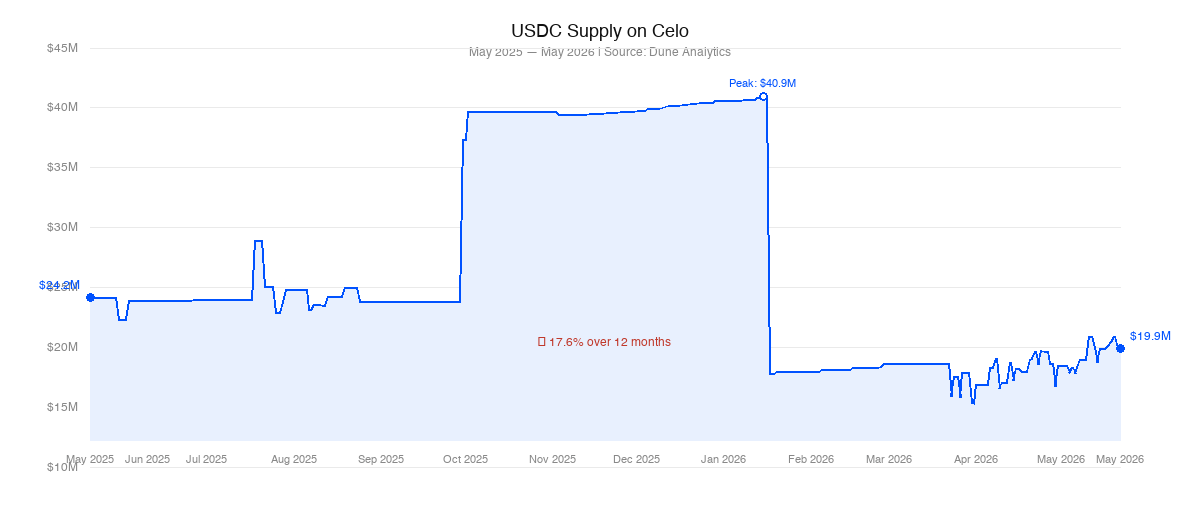

Look down the list of chains where USDC grew. None of them are positioned for African retail. The closest the dataset gets is Celo, the EVM chain originally designed around mobile-first African payments and the home of most local-currency stablecoins from Mento (NGNm, GHSm, KESm, XOFm, ZARm, COPm, BRLm).

USDC on Celo ended the year at $19.9 million, down from $24.2 million. The headline 17.6 percent decline is the least interesting part of the chart. Between September 2025 and January 2026, supply on Celo nearly doubled to a peak of $40.9 million. That peak was mostly one wallet. On January 16, a single unlabeled address, 0xbc7c...3fec, held $26 million of USDC on Celo. The next day, that wallet pulled $23 million in a single move. About $22 million left the Celo chain entirely, bridged or burned off-network. Whoever this is, they kept $3 million on Celo at the time and have since trimmed to $1.88 million.

That isn’t a chain-choice story. It’s a distribution story. Africans hold and move USDC the same way they hold and move USDT, which is through centralized exchanges and peer-to-peer over Tron and Ethereum, off-ramped to bank accounts through fintech apps like Bitnob, Yellow Card, Busha, Quidax, and increasingly the consumer wallets Opay, PalmPay, and Kuda that don’t yet natively support USDC at all. Circle isn’t shipping a product designed for that workflow. USDT got there first and locked in distribution.

I covered the wider local-stablecoin picture in the non-USD scoreboard piece last week. Every EUR, GBP, NGN, ZAR, KES, GHS, BRL stablecoin combined totals about $2.96 billion. That’s 3.7 percent of USDC alone. The local-currency strategy isn’t winning, and dollar stablecoins are filling the vacuum. In Africa, that vacuum has been filled almost entirely by USDT on Tron.

This isn’t a regulatory gap either. Nigeria has the SEC ARIP framework running through 2026, South Africa has FSCA crypto licensing, Kenya is iterating its VASP regime, the EU’s MiCA makes EURC the cleanest regulated EUR stablecoin on the continent. The product gap is distribution into local fintech, not policy.

The growth lever

If you’re an operator at Circle reading on-chain data, there are three asymmetric moves that the year-on-year chart is begging for.

The first is fixing Celo or picking its successor. Celo is the only Africa-aligned chain in the entire dataset and USDC there lost 18 percent in a 31-percent-growth year. Either re-engage with Mento and the Opera MiniPay team to make USDC the default dollar on Celo, or be honest that Celo lost the chain race and push for Base as the African retail home. Base has Coinbase Wallet. Coinbase Wallet ships in Nigeria. The integration surface is smaller, and the user base is already there. The only catch is that the Coinbase team that owned Base’s African go-to-market got reorganized out in the May 2026 layoffs, so what Base’s Africa strategy actually is right now is anybody’s guess.

The second is plugging Circle Payment Network into the African consumer remittance corridor. Nigerian diaspora remittances reached $23 billion in 2025, the highest in five years. The wider Sub-Saharan Africa region received about $55 billion in remittances in 2024 per World Bank data, with senders in Europe, the US, and the UK as the biggest source markets. CPN is positioned for institutional rails, but the volume that matters in Sub-Saharan Africa is consumer cross-border. The play is partnership with LemFi (which just took Tether’s strategic investment), MoonPay, Onafriq, Flutterwave, and the four major Nigerian crypto apps. Put USDC on the receive side of UK-to-Lagos, EU-to-Dakar, US-to-Nairobi. The architecture options are open. The decision to ship is the gating step.

The third is EURC into the Europe-to-Africa corridor specifically. EURC sits at roughly $502 million in supply and at 37 percent of the entire global EUR stablecoin universe. Sub-Saharan Africa is the most expensive receiving region in the world, with average remittance cost of 8.78 percent per the World Bank’s Q3 2025 Remittance Prices Worldwide report, against a global average of 6.36 percent. EURC on the send side, USDC or a local naira / cedi stablecoin on the receive side, settled through a partner, is a payments primitive that nobody else can ship at this scale because nobody else has MiCA approval on a regulated EUR token. This is where the regulatory moat translates into product advantage and where Circle’s competitive position is genuinely defensible against Tether.

What I’m paying attention to

Three things will tell me whether the African gap is closing or not over the next two quarters.

The first is USDC supply on Celo. If it stays below $25 million through Q4, that integration is dead and Circle has effectively conceded the Africa-aligned EVM chain. If it doubles, somebody’s making it work.

The second is whether any of Bitnob, Yellow Card, Busha, or Quidax ships a “send USDC” feature with explicit Circle Payment Network integration. The press cycle for a deal like that is unmissable, and the on-chain data shows the integration immediately as a labeled treasury wallet starts accumulating.

The third is the EURC supply curve. EURC at $502 million is the most concentrated bet on regulated non-USD stablecoin distribution anywhere. If it crosses $1 billion in the next six months, the MiCA strategy is working. If it stays where it is, the regulated-EUR thesis needs revisiting.

The dollar isn’t getting smaller in Africa. The question is whether USDC, which has all the regulatory and product advantages, can take meaningful share from USDT, which has the distribution. The data right now says USDC has not yet started that fight. The next twelve months are when it has to.

Disclosure: I don’t hold CRCL or USDC at material size. All on-chain data is from Dune Analytics queries linked in the frontmatter. Stock data is from Yahoo Finance and CNBC, as of May 22, 2026. This is one person reading on-chain data, not investment advice.