Nathan Allman built the brokerage the rest of the world didn't have. He was 32.

An obituary, a chart, and a brokerage explicitly built for the rest of the world.

I try to read the obituaries every other week. Not because I’m morbid, but because death has a way of putting things in perspective. Today. Today I woke up to news of someone I followed and admired.

Nathan Allman, founder and CEO of Ondo Finance, died unexpectedly on May 26, 2026. He was 32. Four years after founding the company, he left behind a tokenization platform holding about three and a half billion dollars in US Treasuries, dollar-yield products, and stocks.

He also left behind something stranger and more interesting: a brokerage explicitly built for people who aren’t in the United States.

Why Ondo existed

Call her Wanjiru. She’s 24, lives in Kileleshwa, works as a product manager at a fintech in Westlands. She’s a composite. Every number in her situation is real. She has about $4,200 saved across a shilling money market fund, a small dollar balance at KCB or Equity, and a chama she can’t easily withdraw from. She wants to own a piece of something that grows. The AAPL she sees in headlines. Maybe NVDA. Maybe just the S&P 500.

In Nairobi, that ambition runs into a wall.

Every path to US stocks costs and waits. The local platforms either give her a basket she didn’t pick or a wallet model with deposit, FX, and redemption friction at each step. The Nigerian-anchored apps expect a BVN she doesn’t have. The international brokers want an international wire, a W-8BEN, and a level of capital-leaves-the-country attention her bank would rather not surface. Every layer takes a cut. Every layer takes a week.

So she does what most of her cohort does. She puts the $4,200 down on a deposit for a quarter-acre in Kitengela, two hours from town. She’ll pay 12,000 shillings a month for the next seven years. The plot is empty. Goats sometimes wander across it. She visits on weekends. She tells her mother, “this is my investment.”

Land doesn’t fractionalize. Land doesn’t pay yield. Land sits.

Most founders in US fintech and crypto would never see Wanjiru. Their addressable market starts in Manhattan and ends in San Francisco. The American consumer is the easiest in the world to underwrite, the compliance frame is mature, the rails work, the dollar is already the local currency. You can charge a 30 basis point margin on a treasury fund and have venture capital arguing for your seat at the table.

Allman went the other way. Ondo Global Markets is explicitly not available to US users. His treasury fund OUSG is gated to qualified institutional clients, but his retail-facing USDY and his tokenized stocks product target investors in Asia-Pacific, Africa, Latin America, and Europe. The product is built outward.

He built Wanjiru something that bypasses the wall entirely. A wallet she already has. A token she can hold. AAPL the way she holds USDT. No BVN. No wire. No W-8BEN. No deposit-FX-redemption cycle. Her phone, a token, and a price that updates with the underlying.

Local players are still in the fight, Ndovu and MyStocks in Kenya, Bamboo and Risevest in Nigeria, EasyEquities in South Africa, each solving a piece of the problem inside the legacy stack. Allman’s bet was different. You don’t fix the stack. You go around it. A token on a public blockchain, backed by US-custodied stock, isn’t subject to the same friction. The compliance lives in the issuance contract, not in every transaction.

Whether Wanjiru ever opens that wallet is a separate question. The thing Allman built points at the problem nobody else in his seat was even looking at.

What the data shows

Three numbers carry most of the story.

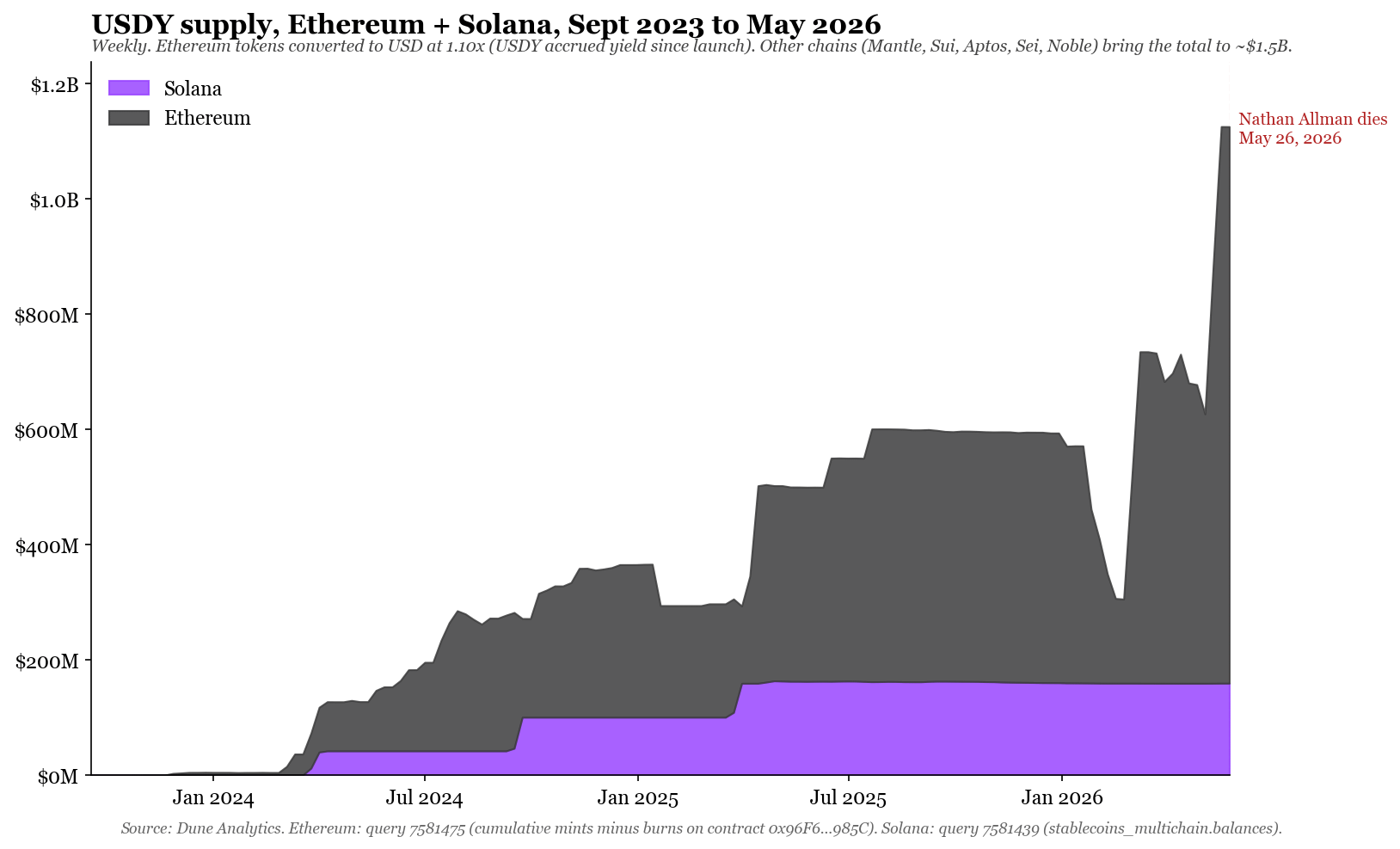

USDY launched in September 2023 on Ethereum and December 2023 on Solana. On-chain, the supply curve looks like the chart above. Ethereum carries the bulk, Solana adds a steady $160 million. Other chains (Mantle, Sui, Aptos, Sei, Noble) bring the total to roughly $1.5 billion by May 2026. The growth wasn’t linear. There’s a wave in mid-2024 to about $250 million, a plateau, then a step-up to $600 million in mid-2025, a dip in early 2026, and a surge to over a billion in the weeks before Allman’s death.

OUSG is the institutional product, now around $693 million in TVL. The on-chain Ethereum-only figure is lower because Ondo migrated significant flow into rOUSG (the rebasing wrapper) and into USDtb, the regulated stablecoin issued through Anchorage Digital under the GENIUS Act. Institutional money is more rotational than retail money. The consolidated treasury exposure is still in the platform, just under different wrappers.

Ondo Global Markets is the newest and the fastest. It launched in September 2025 with around $350 million in TVL within the first months. It crossed $1 billion in TVL by mid-May 2026, eight months from zero. By the time Allman died, the platform was running tokenized versions of NVDA, AAPL, META, TSLA, CRCL, SPY, QQQ, TLT, TIP, AGG and roughly 190 other tickers, available on Solana, Ethereum, and BNB Chain, where the rollout exposed the product to roughly 3.4 million daily active users.

Inside the roughly $19 to $21 billion total RWA market, Ondo’s three and a half billion is meaningful. Inside the tokenized equity sub-category, 70 percent of the supply runs through Ondo’s contracts. One protocol, one founder, one team. The tokenized stock market has a winner-take-most shape that the dollar stablecoin market also has, and the seat Ondo occupies in equities now is structurally close to the seat Tether occupies in dollars: not the only player, but the one everyone else benchmarks against.

The BNB Chain rollout is the part of this story that most US-coded analysts are missing. BNB Chain has the highest daily active user count of any chain that isn’t Solana or Tron, and a meaningful share of that activity is in markets where Coinbase, Robinhood, and Schwab don’t operate. When Ondo Global Markets shipped on BNB Chain, it exposed 200 tokenized US stocks to roughly 3.4 million wallets that were never going to download Schwab. That’s the access bet operationalized.

What he was building toward

The longer arc was bigger than the three products. Allman was building toward tokenized everything: stocks, ETFs, bonds, commodities, with Ondo Chain as the settlement layer underneath. The bet, in his own words, was that institutional-grade financial products belong on public blockchains and that compliance is the moat, not the constraint. Public reporting from earlier this year described the strategic positioning around “global financial access” as a deliberate evolution from the original treasury-tokenization thesis.

The work isn’t done. He had open partnerships with BlackRock‘s BUIDL framework, with Securitize, with custodian partners across Asia. He had Ondo Chain in development. He had a roadmap that named tokenized real estate, tokenized commodities, and tokenized money market funds. He was building a tokenization stack the way Stripe built a payments stack, with the products plugging into one settlement spine.

The platform now has the products it needs to outlast the founder. That’s not a small thing. Most early-stage crypto companies are person-shaped: the founder is the product, the network, and the conviction. Ondo crossed into product-shaped sometime in 2024. The on-chain numbers can keep growing under Ian De Bode even if the conviction takes longer to rebuild.

What happens next

De Bode was Ondo’s longtime president. He oversaw strategy, product, and daily operations. The succession is clean by crypto standards: no founder dispute, no token whiplash, no exit by the senior team. The Ondo press release confirming Allman’s death also confirmed his appointment, with the backing of the leadership team.

The open question is institutional retention. OUSG holds BlackRock-adjacent capital that’s there because of a specific compliance and credit story Allman told. USDY holds regulated counterparties who underwrote Ondo’s controls. Both flows will be tested in the next four quarters by counterparties asking, quietly, whether the founder-shaped trust extends to the new leadership. The early read should be yes given De Bode’s tenure and the depth of the team. But it’s a real test.

The Kenyan retail user on Global Markets won’t notice any of this. The mint and redeem rails keep working. The 200 tickers stay live. The product, for the people Allman built it for, doesn’t change.

A short close

I followed Allman’s work because he was solving a problem most people in his seat didn’t even see. The Treasury tokenization story everyone talks about at conferences was the easy part. The Kenyan twenty-something who buys her first AAPL through a wallet in 2027, instead of putting that money into a half-acre outside Nairobi, is the part nobody else was building for. She won’t know his name. He’d probably prefer it that way.

Disclosure: I don’t hold ONDO, USDY, or OUSG, and I haven’t held them in the past 12 months. All on-chain data is from Dune Analytics, queries 7581475 (USDY Ethereum) and 7581439 (USDY Solana). Aggregate TVL figures are from public Ondo and press-release sources cited above. This is one person reading public data and an obituary on a Tuesday morning.