There are 217+ stablecoins now. The 65 that don't track the dollar hold about 1 percent of the supply.

I pulled every non-USD stablecoin from Dune's dataset. EUR and RUB are neck and neck at the top, and one issuer carries the entire emerging-market long tail.

Dune now tracks 217 stablecoins across 38 chains. The 65 that don’t track the dollar hold roughly 1 percent of the supply between them.

When Dune launched its Stablecoins collection with Steakhouse Financial in February, the headline feature was attribution: every transfer classified by intent, every address bucketed by use case (CEX, bridge, lending, yield, treasury, whale, and so on). The genuinely interesting story, though, is buried in the metadata. The unified stablecoins_multichain.tokens table is a directory of every stablecoin Dune now indexes, with the ISO currency code each one pegs to. I queried it expecting the long tail to be sparse. It’s worse than I thought.

How big the non-USD universe actually is

The Dune dataset covers 26 ISO currency codes. The breakdown:

USD: 152 distinct tokens. USDT alone is around $190 billion in circulation, USDC about $79 billion. The biggest of the dollar stables is roughly 120 times larger than every non-USD stablecoin combined.

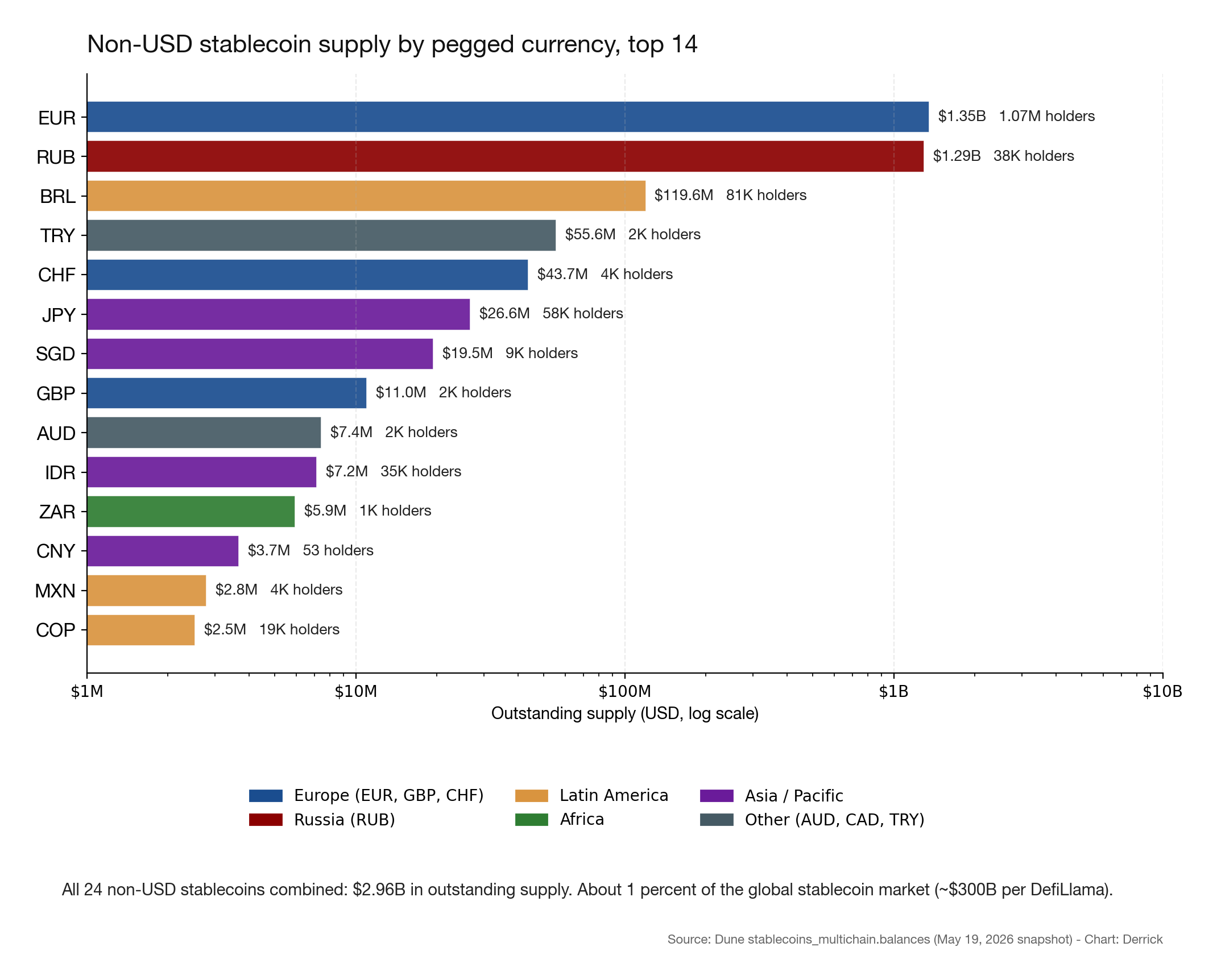

EUR: 18 tokens (EURC, EURS, EURT, EURA, EURI, EURAU, EUROe and a dozen more). $1.35 billion in supply, 1.07 million holders. The only non-USD ecosystem that looks remotely like a real ecosystem.

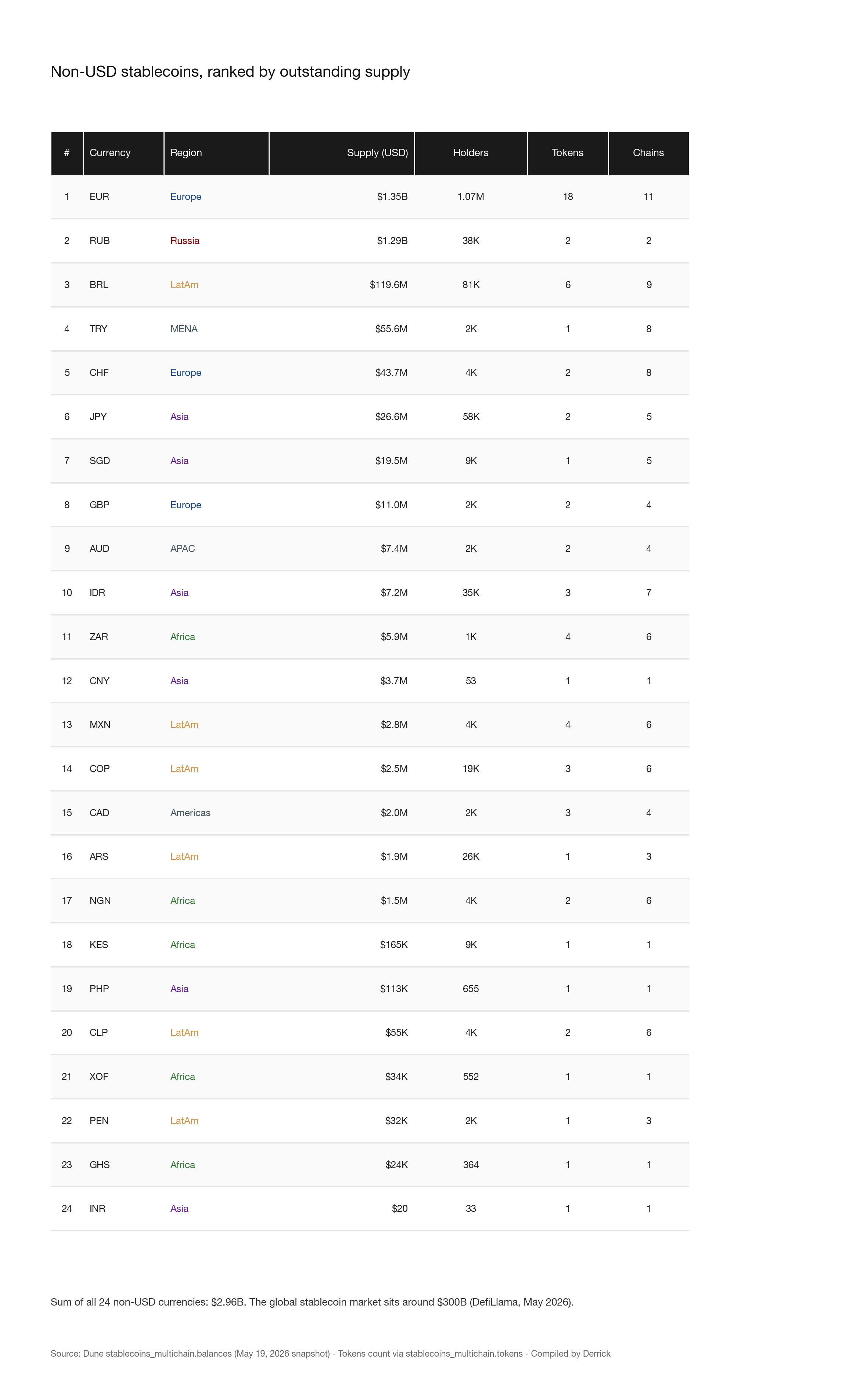

BRL, ZAR, MXN, CAD, COP, IDR: 3 to 6 tokens each.

GBP, JPY, AUD, NGN, CLP, RUB, CHF: 2 tokens each.

CNY, ARS, SGD, TRY, GHS, KES, PHP, INR, KZT, XOF, PEN: one token each. Most are running on a single chain.

Total non-USD stablecoin supply, all 24 currencies that currently have any outstanding balance: $2.96 billion. According to DefiLlama, the global stablecoin market sits around $300 billion in May 2026. Non-USD is therefore about 1 percent of the universe.

The full scoreboard:

The two surprises at the top

Read the top of the table again. EUR and RUB are within $58 million of each other on outstanding supply: $1.35 billion versus $1.29 billion.

EUR makes sense. It’s a $300 billion regulated stablecoin opportunity in waiting, the MiCA framework is now live across the EU, Circle‘s EURC has serious institutional pickup, and an 18-token issuer landscape means real competition. A million-plus holders distributed across 11 chains looks like infrastructure forming.

RUB doesn’t make sense in the same way. There are two RUB stablecoins in the dataset (A7A5 and wA7A5), 38,000 wallets hold them, and they’re on exactly two chains. One currency, two tokens, almost all of it sitting in a handful of treasuries. The supply matches EUR’s. A7A5 is widely understood to be Russia-aligned settlement infrastructure built to route around sanctions, and the data tells that story cleanly. Big balance, very few holders, very few tokens, very few chains. That’s not a retail ecosystem. That’s a wholesale rail.

Two stablecoins, near-identical supply, near-opposite distribution. Same row of the same table.

The Mento footprint

Look at the symbol list for the smaller currencies. NGN has cNGN and NGNm. Ghana has GHSm. Kenya has KESm. The West African CFA franc has XOFm. Colombia has COPm. Brazil has BRLm alongside the local Brazilian-issued BRLA, BRL1, BBRL, BRZ, and wBRL. Philippines has PHPm. The “m” suffix is Mento Labs, the on-chain stablecoin protocol that originated as the stablecoin layer for the Celo blockchain.

One issuer carries most of the emerging-market long tail. Some implications:

For the African countries where Mento is the only option (GHS, KES, XOF), the “local stablecoin” market is essentially one Mento contract, one chain, a few thousand wallets. That’s not a country-level rail. It’s a pilot, and pilots can disappear with one regulatory call.

For Nigeria, which has both cNGN (Convexity-led consortium) and NGNm (Mento), the two products together still total around $1.5 million in supply distributed across roughly 3,700 wallets. I wrote about cNGN’s growth at length last week, and it’s the live case study in what early traction looks like for a regulated local stablecoin. The Dune data slots it into context here as the 17th largest non-USD stablecoin globally. Bigger than KES, smaller than ARS. That’s the actual scale.

For Brazil and Mexico, where there’s competing local issuance (BRLA, BRL1, BBRL, BRZ for BRL; MXNB, MXNe, MXNt for MXN), the local issuers are growing faster than Mento and starting to capture real holder counts. BRL has 81,000 holders and $120 million in supply. That’s a real economy.

Where this leaves the cNGN argument

If you’re trying to build a regulated naira (or cedi, or shilling, or peso) stablecoin, the data has uncomfortable news. The category as a whole is a rounding error. Every entrant currently below $5 million in supply is, by global stablecoin standards, statistically zero. There are no scale advantages, no liquidity flywheel, no incumbents to displace because the incumbents themselves are also at pilot scale.

This actually makes the cNGN bet more interesting, not less. The greenfield argument writes itself: a regulator-blessed, multi-chain, Africa-focused stablecoin is the bet that any of these emerging-market local rails could be the one that breaks out. The aggregate market is small, the median project is one Mento contract on Celo, and the player who gets distribution into local fintech (Opay, PalmPay, Kuda in Nigeria; Pix-integrated wallets in Brazil) gets a shot at being the de facto naira-on-chain.

The competing argument is uglier. Maybe the reason non-USD stablecoins are 1 percent of the market isn’t a distribution problem. Maybe it’s structural. Most people who want to escape a weak local currency already have the option of holding USDT or USDC, which is exactly what the data on Tron and Base shows happening across Africa, Latin America, and Southeast Asia. A regulated NGN stablecoin solves the regulatory clarity problem, but it doesn’t solve the “your currency is losing 30 percent per year against the dollar” problem. The dollar stables solve that one by existing.

I don’t think it’s actually structural. The Brazilian numbers (real holder distribution, multiple competing issuers) suggest that when local fintech genuinely integrates and the local payment rails are good, a local stablecoin can find users. But the structural-doubt argument needs an answer, and the data right now isn’t refuting it.

What I’m paying attention to

Three things I’ll be watching over the next six months.

The first is the EUR ceiling. EUR is the only non-USD stablecoin category with real ecosystem behavior: $1.35 billion in supply, more than a million holders, 18 competing issuers, MiCA-cleared distribution into European fintech. If EUR stablecoin supply doesn’t cross $5 billion by Q4 2026, the “regulated non-USD stablecoins are a real product category” thesis has a hole in it that’s not actually about Africa or Brazil.

The second is the RUB number. If RUB stablecoin supply keeps growing while holder count stays near 38,000, that’s wholesale settlement scaling under sanctions. If it stops growing or contracts, sanctions are biting. Either way, A7A5 is one of the more honest reads available on cross-border value movement in Russia, and Dune now publishes it.

The third is whether any single emerging-market local stablecoin crosses $10 million in supply with at least 50,000 holders. Today none does. cNGN, MXN, and IDR are all under that threshold on at least one of the two axes. BRL is the only emerging-market local stablecoin that has crossed both, which is why the Brazil story matters. That’s the bar that distinguishes “this is a pilot” from “this is a product.” The first one to cross it sets the playbook for everyone behind them.

The dollar’s 99 percent isn’t going anywhere in 2026. The interesting question is whether the 1 percent stays a rounding error or starts to fragment into a real multi-currency map.

Disclosure: I hold small positions in some of the stablecoins discussed above, none at material size. All data is from Dune Analytics's stablecoin dataset queries, linked above. Market totals are cross-referenced against DefiLlama. This is one person reading a Dune query, not investment advice.